Our Team will be in Las Vegas from Jan 31 to Feb 2 for the International Builders Show, National Hardware Show and Surfaces conferences. Reach out to us if you want to connect!

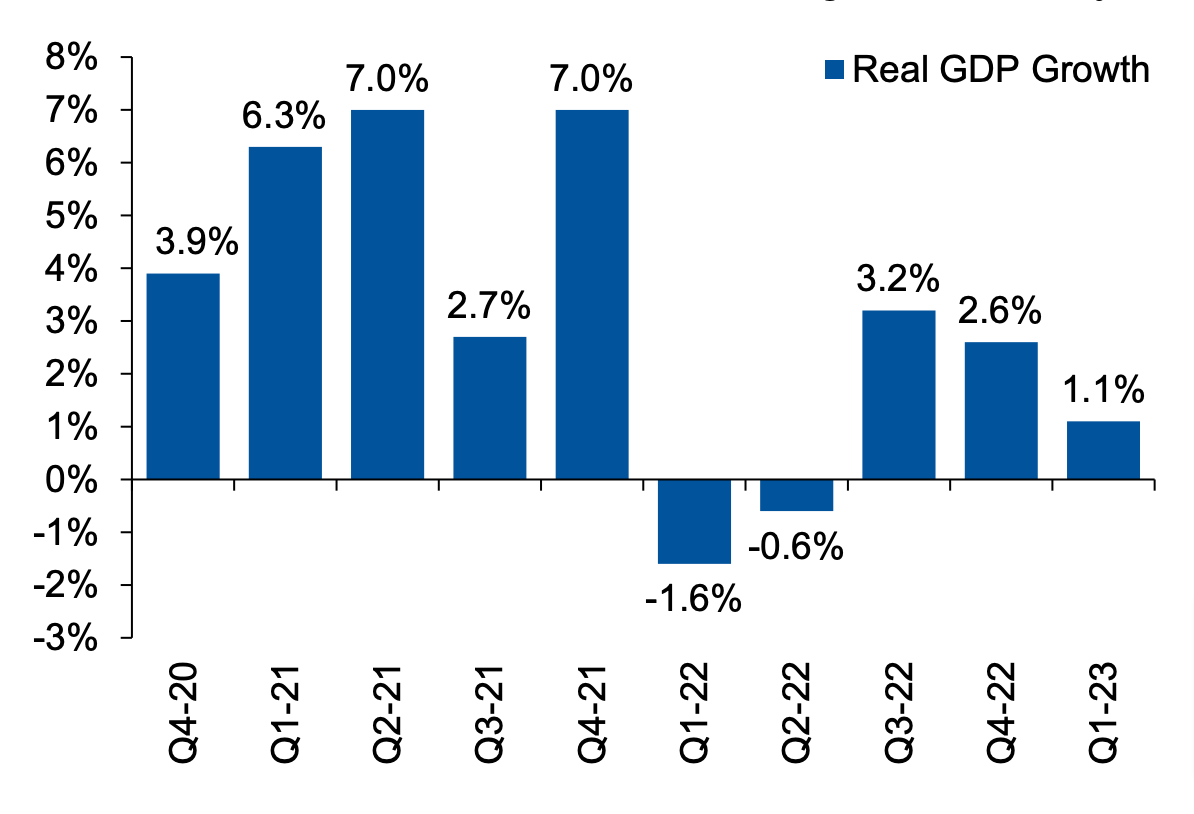

The U.S. economy is in a state of transition as it continues to slow from the torrid pace during the post-COVID recovery but remains resilient despite an aggressively hawkish Fed which continues to increase the fed funds rate and tighten monetary policy. Rapidly rising interest rates have dampened consumer demand which is evidenced through residential new construction and is beginning to have an impact on commercial new construction activity. Conversely, activity associated with the service, maintenance, and remodeling of the residential or commercial installed base has remained robust and should continue to grow as the underlying demand is more nondiscretionary and not as prone to cyclical demand shocks as new construction. HVAC, Plumbing, & Electrical (HVAC/P/E) contractors with greater exposure to new construction activity will likely see a mixed growth outlook in the near term, depending heavily on their geographic presence and end market exposure. Contractors focused primarily on service, maintenance, and repair should continue to see steady, healthy growth even in a slowing economic environment.

M&A Tailwinds

Long term, there are several strong favorable tailwinds to support increased demand and facilitate growth for the foreseeable future for the HVAC/P/E trades. Outlined below are some of the key themes owners should consider capitalizing on to enhance shareholder value and why the buyside community, particularly private equity, views this space as a compelling investment thesis.

Inflation Reduction Act

The Inflation Reduction Act of 2022 (IRA) provides a number of tax credits and rebates for homeowners who make energyefficient upgrades to their homes, such as installing new HVAC systems, water heaters, and appliances. These tax credits and rebates will help to offset the cost burden of these upgrades making them more affordable for homeowners which in turn will provide a positive catalyst to growth for HVAC/P/E contractors. It is worth noting this is the most significant change to federal energy efficiency tax credits and rebates in many years and the benefits of which extend for the next ten years.

Refrigerant Transition

The HVAC industry is undergoing another refrigerant transition as the Environmental Protection Agency (EPA) is phasing out the use of hydrofluorocarbons (HFCs) which are regarded as high global warming potential (high-GWP), such as R-410A and R-404A, in favor of new, low-GWP alternative refrigerants, such as R-32 and R-454B. Starting January 1, 2024, the industry will see a 40% reduction in HFC production which makes 2023 a pivotal year in preparation for the transition. For contractors, this presents a challenge to train technicians on the new refrigerants, particularly as many of these new refrigerants are mildly flammable so additional care is warranted. On the other hand, the refrigerant transition presents a significant opportunity longer term for contractors. As the old, high-GWP refrigerants are phased out of production the material costs will inevitably increase over time and, eventually, consumers will be forced to upgrade to more energy efficient units as the economics of servicing legacy equipment with the high-GWP refrigerants will become too costly.

Aging Housing Stock – Zonda

Aging Infrastructure

The U.S. owner-occupied housing stock is aging rapidly as new residential construction continues to lag behind an increasing population and new household formations. An interesting stat to highlight is the median age of owner-occupied homes is now over 40 years. Nearly 50% of homes were built before 1980 and only 10% were built since 2010. This presents another opportunity for contractors to capitalize on the aging installed base of housing in the U.S. as more and more units reach the end of its useful life each year and will inevitably need to be replaced.

M&A Headwinds

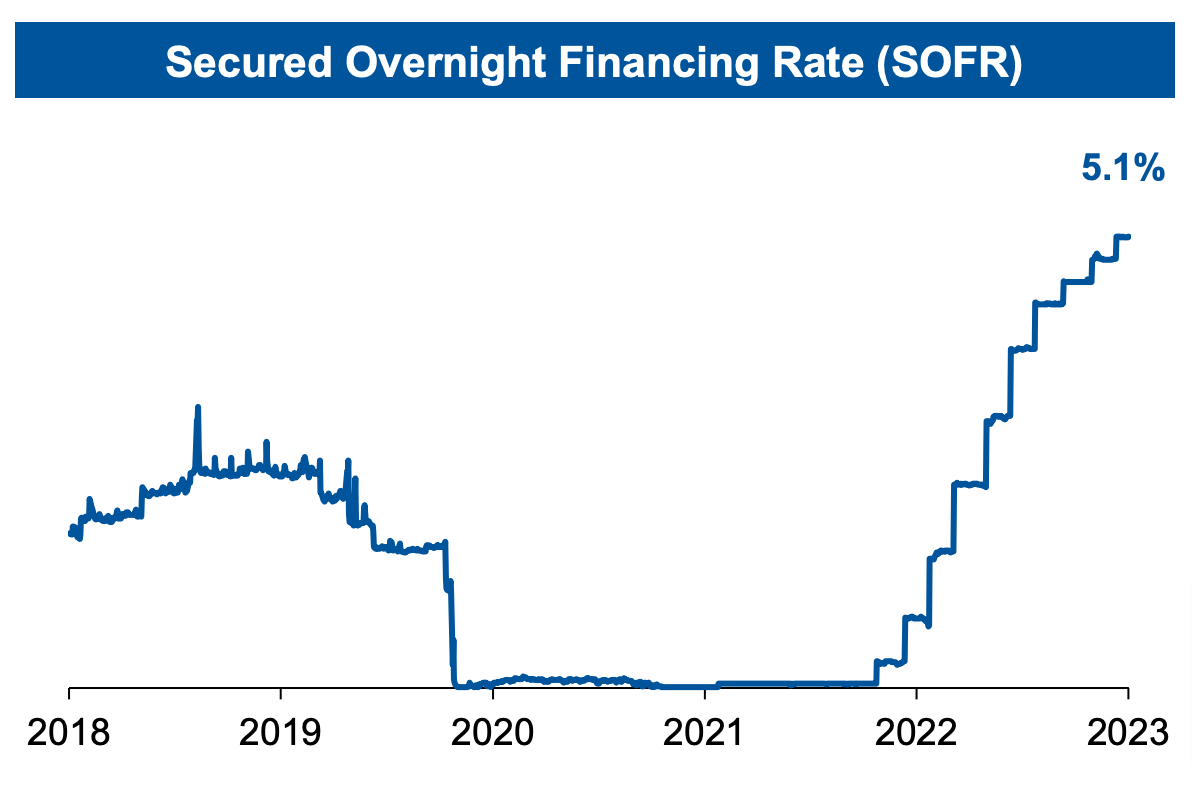

Rising Interest Rates

SOFR – Federal Reserve Bank of New York

Rising interest rates and the rerating of the cost of capital since the Federal Reserve began its interest rate hiking campaign a little over a year ago has started to take its toll on M&A activity. In late 2020 and through 2021 during the post-COVID recovery when the fed funds rate was anchored at zero and financial conditions continued easing, M&A activity exploded and, in some cases, valuation levels reached frothy levels. Lenders were willing and able to underwrite with stretched leverage multiples and low interest rates as most deals would “pencil” in that environment. Today, we see a world where the Fed has increased the Fed funds rate by 500 basis points in a year, spreads have started to widen, and lenders are pulling back leverage multiples by a full turn or two. Lenders nervous about their deposit base have significantly pulled back on financing transactions, although private credit with a stickier capital base have continued extending credit to facilitate M&A transactions, albeit on “lender friendly” terms.

What does all of this mean for M&A activity in the HVAC, plumbing, and electrical space? Overall activity has slowed and will continue to remain below peak 2021 volume. High quality assets with strong management teams will continue to attract buyers and receive financing but the next level down in the quality spectrum could be challenged. Valuation levels will cool off as buyers, particularly private equity, are challenged to lean in on value with lower leverage and increased cost of capital. For certain situations, financial sponsors are likely to find themselves in a position of cutting a larger equity check or risk losing a deal altogether. Bottom line – It’s not all doom and gloom because interest rates are at the highest level in over 15 years. It’s a different environment from 2020 and 2021, and expectations on valuation and overall activity should be recalibrated for a high interest rate world.

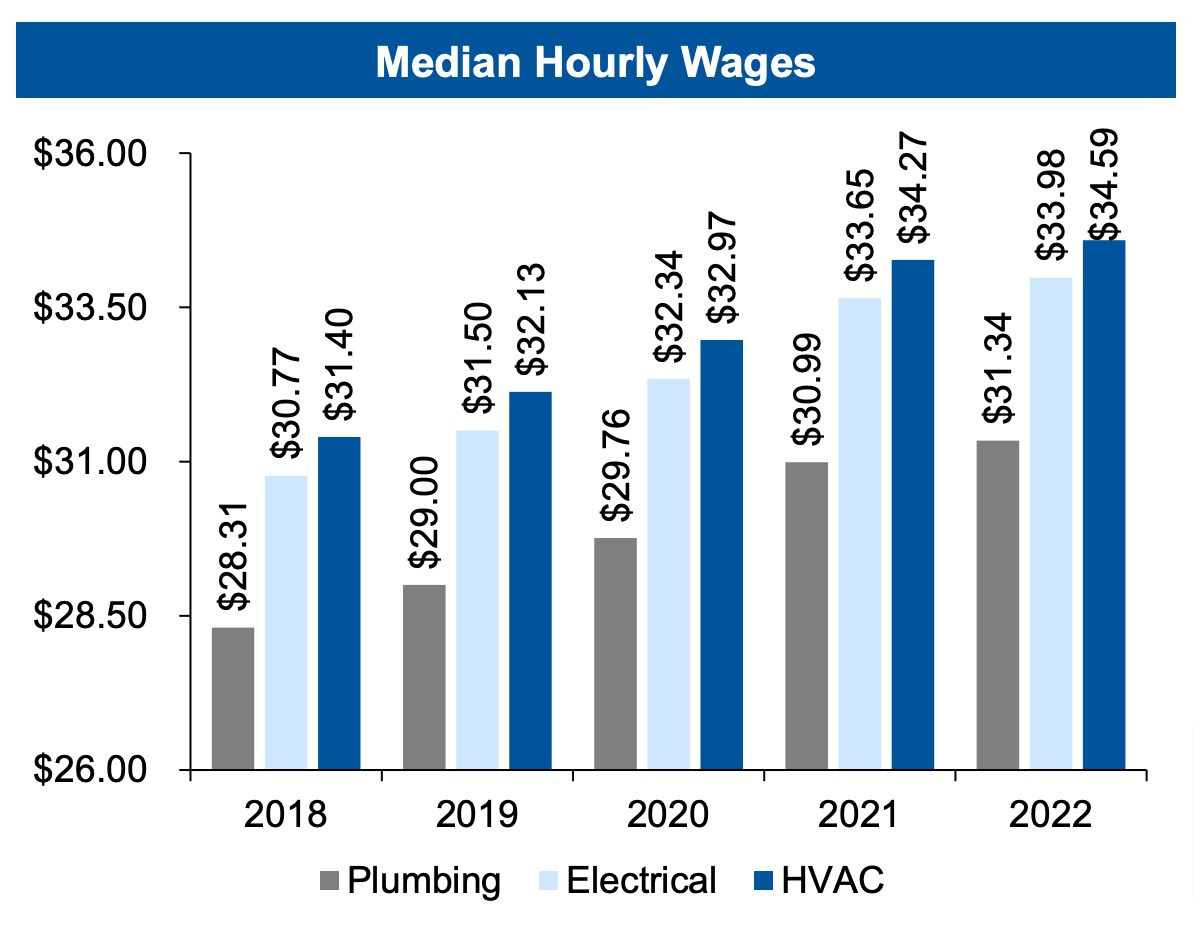

Median Hourly Wages – U.S. Bureau of Labor Statistics

Hiring & Retaining Skilled Labor

The #1 issue facing contractors in the trades right now is hiring and retaining skilled, qualified technicians. Short term, there are limited solutions to the problem as a greater number of older employees retire every day versus newer, younger entrants into the trades. This labor supply and demand imbalance will continue to add to inflationary wage pressures as employers seek to retain seasoned technicians. Longer term, there’s a coordinated effort in the industry to encourage the younger generation to consider a career in the trades as an alternative career path. Many of the larger contractors have established training programs and academies to train the next generation of technicians to backfill the coming wave of retirements from the older generation.

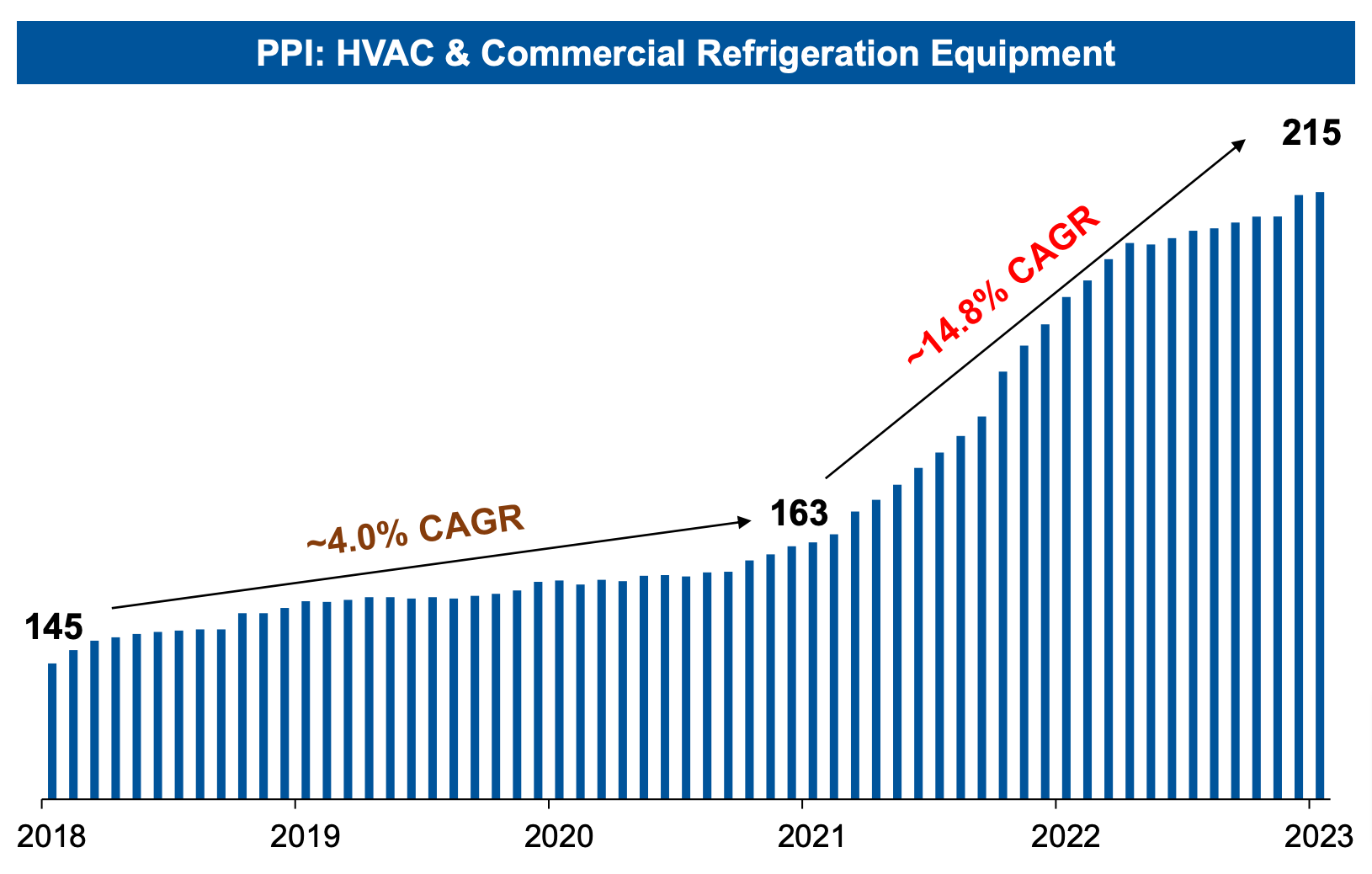

PPI – U.S. Bureau of Labor Statistics

Inflationary Cost Pressures

The HVAC, plumbing, and electrical industry has, like nearly every other industry, faced inflationary cost pressures for the last couple of years and, while there are some signs of disinflation working through the system, it appears this time inflation is stickier than in years past. Rising labor costs, particularly with technicians, continue to be a primary culprit of the inflationary pressures. Given the scarce pool of qualified technicians coupled with increasing demand, there is a war for talent taking place in the industry with larger contractors offering sizable compensation arrangements to technicians, further exacerbating the problem. Material costs have further contributed to the inflationary cost pressures driven in large part by the supply chain bottlenecks and parts shortages coming out of the post-COVID recovery. Most contractors have combated the recent inflationary headwinds by passing along price increases to customers, which can be effective in maintaining margin, but there are other levels to pull in addition to raising prices.

Look at your cost structure and identify opportunities to squeeze out savings. Many of larger contractors of scale have started to use their weight with vendors and have negotiated more favorable pricing terms. Another option is to evaluate the cost efficiency of how labor is utilized, such as route optimization for technicians in the field.

M&A Activity

M&A Volume – S&P Capital IQ, Proprietary Anchor Peabody Closed Deal Data

Current Environment

M&A activity for HVAC, plumbing, and electrical contractors has been extraordinarily robust for the last several years. While overall activity has slowed recently, due in large part to rising interest rates and uncertainty around the growth trajectory of the economy, M&A activity has moderated to a more normalized pace. Most industry participants would agree the deal activity for the ~18 months prior to 2023 was unsustainable and a moderation in M&A volume was expected. It will be interesting to see how the back half of 2023 plays out if the recent rerating of the cost of capital remains elevated and we see a material slowdown in the economy.

Private equity continues to play an outsized role in M&A activity in the space with little sign of slowing down. In fact, there over 70 private equity-backed platforms in the residential space and another ~30 in the commercial & industrial space. The number of platforms seems to increase by the month as more and more smaller firms enter the M&A roll up game and form a new platform to consolidate smaller independents. That said, there remains enormous opportunity for further consolidation given how highly fragmented the space is today.

The consolidation playbook and strategic angles vary by firm and platform, but common themes have emerged:

New construction vs. service, maintenance, & repair: By and large, nearly every platform is staying away from any exposure to new construction. Some have comfort up to ~20% of the business tied to new construction but anything materially more than that level will be a challenge to stomach for most of these players. This presents a tremendous opportunity for those platforms comfortable with new construction as competition for acquisition opportunities won’t be as crowded as the service and maintenance opportunities.

Residential vs. commercial: Private equity-backed platforms and overall interest is certainly over-indexed to residential but that’s not to say there’s a lack of focus on the commercial and industrial space. There are few dynamics that make residential a compelling investment thesis, such as low cash conversion cycles, pricing power with the customer base, and overall, less complexity to name a few, which lends itself well to most private equity playbooks. Although, commercial and industrial provide large project jobs and backlogs of work over time which gives good visibility of earnings potential over the next 12 to 18 months.

Geographic footprint: The sunbelt region, particularly the southeast, remains the focus of most of the platforms consolidating the space and continues to demonstrate an elevated level of competition for quality assets. Taking it a step further, the independents situated in coastal communities in the southeast are one of the hottest commodities right now.

Capabilities and service offering: One question that is commonly asked – Do we need exposure to more than one trade? The short answer, not necessarily. All the super-regional or national platforms have the three trades under one roof but it’s not uncommon to see the smaller, regional platforms with exposure to only one or two of the trades. HVAC is the most common of the three followed closely by plumbing but this is largely a reflection of composition of the total addressable market.

M&A Outlook

The back half of 2023 should remain active but at volume levels below those seen over the last couple of years. The M&A environment remains exceptionally favorable to sellers as institutional capital continues to find its way into this space and, in our opinion, the flow of capital will accelerate if the U.S. heads toward a recession in the coming quarters. Institutional capital will seek out nondiscretionary, recession resilient industries to “hide out” during an economic downturn and the HVAC, plumbing, and electrical trades check all the right boxes. This flow of capital will likely offset any challenging headwinds from high interest rates, particularly for smaller independent transactions, and keep a bid on valuation to an extent. Looking out to 2024, we are anticipating one of the most compelling opportunities for owners considering selling their business. The large private-equity backed platforms will continue to be active as most begin entering the late stages of their hold period which is typically 3 to 5 years. The reason 2024 presents a unique opportunity for owners considering a sale is because by 2025 and 2026 many of these platforms will transition from buyers to sellers. After 2024, we are expecting a wave of supply to hit the market as most of the platforms formed or acquired in 2020 and 2021 will seek to exit, nearly all at the same time. With that said, if you’re an owner considering a sale in the very near future, it would behoove you to consider transacting over the next 12 months to get in front of the coming wave. When you have an environment, like we expect in 2025 and 2026, where a disproportionate number of large buyers become sellers, you’re removing a significant amount of demand from the market and you as a seller get caught up in a crowded field. As a seller, you want to be in a market with strong buyer demand and limited supply of quality assets which is the backdrop for the remainder of 2023 and into 2024.

About Anchor Peabody

Anchor Peabody is an investment banking firm with a 100% focus on the U.S. building and construction industry. As one of the largest building industry-focused teams in the country, our team has over 100 years of capital markets and mergers & acquisition experience and the wisdom of decades of experience as owners, operators and investors in the space. The Anchor Peabody model is a modern approach to investment banking designed to deliver outsized results for our clients via our granular industry knowledge, complete interest alignment with client objectives, and an employee-first culture. For more information, visit anchorpeabody.com.